Outlining the recently-enacted Social Security Fairness Act

By SCOTT WIMMER, CFA, CFP®, EA

Meredith Wealth Planning

On Jan. 5, 2025, then-President Joe Biden signed into law the Social Security Fairness Act. The new law effectively eliminated the Government Pension Offset & Windfall Elimination Provision. These provisions affect roughly 6% of the workforce whose earnings are considered non-covered for Social Security purposes.

How does Social Security work? ‘Covered’ vs. ‘Non-covered’ earnings

95% of workers contribute to Social Security every year via the OASDI tax on their paycheck. This tax is 12.4% of your gross earnings and is often split between employee and employer. The program is a “pay-as-you-go” system where the current workforce is paying for current Social Security benefit recipients.

As noted above, 95% of the workforce pays into the program and are considered to have “covered” earnings. Covered earnings imply that an individual paid into the program while working; thus, qualifying them for a benefit at retirement. The remaining 5% of the workforce are considered “non-covered” from an earnings standpoint as they do not pay into Social Security from those earnings. This small group includes many government employees, first responders and public-school workers.

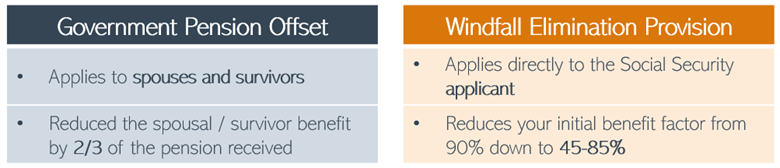

GPO & WEP – What are they?

In 1983, Congress passed new laws to shore up the financial health of the Social Security program and prevent “non-covered” earners from qualifying for benefits. Today, the Social Security Administration estimates that nearly 3 million retirees are affected by these provisions.

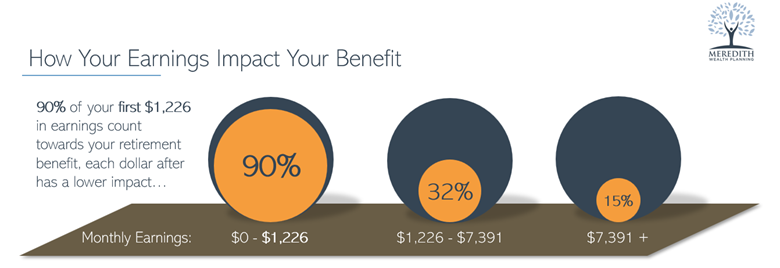

The primary reason behind the new law was driven by how Social Security benefits are calculated. The details are beyond the scope of this article; however, below we can see how Social Security replaces a higher portion of your income with a smaller portion of your covered earnings. This feature benefits low-income earners and qualifies them for larger benefits upon retirement.

You will notice that 90% of your first $1,226 of earnings will go towards calculating your benefit. Once an individual is making over $7,391, only 15% of those dollars are taken into consideration.

How This May Affect You & Steps to Take

Illinois is one of 12 states where public pensions do not contribute to Social Security; the National Education Association estimates that over 105,000 Illinois residents will be impacted by the new law.

- Check your earnings record – It is always good practice to double–check your earnings record on file with the Social Security Administration. This is crucial for those retirees who have worked part-time jobs after retiring.

- Families & Beneficiaries – The GPO elimination means that many families now qualify for a benefit via a spouse or family member. Prior to the law, these families may have had their spousal / survivor benefits eliminated by the GPO provision. Many families may be unaware of the new laws and are under the belief that they will never qualify for a benefit from the program.

- Plan for Additional Taxable Income in Coming Years – The new law is retroactive for 2024 meaning that individuals who are now entitled to a benefit will receive backpay from Social Security. There is no need to contact the local SSA office to claim the benefit. It may take the administration some time to properly implement these benefits. This back pay for benefits owed may increase taxpayer’s incomes in 2025, 2026 and beyond. This added income needs to be considered to avoid unwanted tax impacts down the road. As much as 85% of your social Security benefit may be taxable each year based on your income.

- Review Your Filing Strategy – If you haven’t filed for Social Security yet, you may want to revisit your original plan based on updated figures if GPO & WEP impacted your benefits. Even those who have filed within the past 12 months may want to reconsider their decision and withdraw their claim.

- Plan For Reduced Benefits Down the Road – The elimination of GPO & WEP accelerates the financial strain on the Social Security program. According to new projections, the Social Security trust fund may be depleted by 2032 now if Congress fails to act. If Congress fails to act and the trust is depleted, recipients should plan on a 21% reduction in their current benefits. Nearly 80% of current benefits will be funded through the payroll tax; however, a reduction in benefits down the road could impact retirees who rely heavily on the monthly benefit.

Lead Financial Advisor Scott Wimmer, CFA, CFP®, EA, joined Meredith Wealth Planning in Maryville, Ill. (6300 E. Main St.) in 2022. He is the lead advisor for all new clients of the firm, and brings extensive expertise on investments, financial planning, and taxes. For further information, call (618) 744-6755 or visit online at https://www.meredithwealth.com/.